In my last several offerings of thoughts on additive manufacturing, I shared some economic perspectives for AM disruptions, some rationales of the AM expensiveness, and some wild guesses on the near future of AM price & cost. AM technology is evolving fast in many ways, and so many passionate & talented people are working hard every day on pushing the limit of this technology (I have met and talked to many on LinkedIn and I am continually being amazed by their achievements). Every step matters, some can be strategically important in the long run, but the other, if happens, might make huge noise for current applications and markets. If you are a technology manager or R&D leader with limited resources on hand, how would you plan the spending budget on different AM projects for the next several years, or

Why or why not priorities certain AM development needs over the others?

This is another question I were asked several times in delivering AM insights to stakeholders of my research. I spent quite several minutes making a list on the scene and tried to “finding” (or creating 😊) a logic behind it (“I am not sure” may not be an affordable answer especially for presentations for my Ph.D. qualify or defense). At that moment, I was less experienced with thoughts that were ill-structured. I believe you would laugh at my old answers if you heard them (because I do, I won’t write down here due to embarrassment, but contact me if you really really want to have this joy). With ages building on, I think I may do better now or at least I know the mighty answer of “it depends”. If I were able to choose what current AM developments to be invested, my first priority would be

AM design and the tool/software used for designing

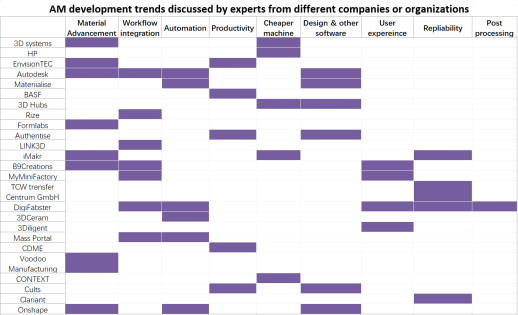

I will explain why from the economic perspective that I shared with you before. Candidates for such questions can be many since AM is developing in different disciplines. I found some good resources with thoughts about the development trends from many experts (Michael Petch interviewed AM CEOs and experts for 2018 trend on 3dprinting.com, Duann Scott’s thought from Autodesk, and Gartner Inc’s prediction). In order to save your time reading them all, I summarize a list from those resources for the AM developments in the near term that mentioned by experts from different background:

Although those experts can only speak for what they are representing, I believe a collective view of the list may not be that subjective. Interestingly, most of those development candidates are directly about the process (automation, productivity, cheaper machine, reliability, post-processing, and maybe workflow integration), which indicates a strong need for more work on a better process. But remember what I emphasized in my discussions about delta profit?

Product, product, product!

AM technology or the process determines the bottom line of the delta profit, which is very important for new markets in a longer timeframe. But short-term speaking, a disruptive product with a higher price tag can impact the delta profit more significantly and faster. It would be strategically smart to find the top line first and raise the bottom line later when the technology catches up. Among those candidates of options, only material advancement, design & other software and maybe workflow integration are directly related to the product. Economically speaking, I will put them as my priorities due to their impact on the product and the delta profit.

From the technical aspects, the hurdles and difficulties that need to be overcome for different development vary a lot. Improvement of the cost performance of the material depends on hard science and scalability, which can be extremely difficult and slow. Similarly, process reliability, automation, and productivity enhancement also need a significant amount of work and even rely on the progress of other emerging technologies such as AI, industry 4.0, and laser tech. Reducing machine price may not be that hard and it is happening right now as I discussed in my wild guesses. Similar to develop an improved design tool with a user-friendly interface. If you put those development needs in a matrix combining technical and economic perspectives, four quadrants form: Quick wins (higher impact, lower effort), Major Projects (higher impact, higher effort), Fill-ins (lower impact, lower effort), and long-term vision (lower impact, higher effort):

Improving AM design and the tool/software used for designing is a quick win for the industry!

Some evidence recently from the moves of major AM players: Desktop Metal announced Live parts; HP partnered with Solidworks; Carbon offered pre-processing software solutions; Ansys acquired 3DSIM; GE acquired GeonX; Autodesk acquired Netfabb;… All about improving the design through better tools.

“Action expresses priorities.” – Mohandas Gandhi

I don’t mean other AM developments are not important. In the contrary, most of them should be the “major projects” and “long-term vision” for the technology and hold the largest potential in changing the landscape of the AM industry. Those require extra effort and still have a long way to proceed. Improving AM design and the tool may generate impact near-term.

Ironically, although the design fundamentally determines the functionality and profitability of the product, they actually stand at each end of the workflow where the design starts first and the product comes out the last. Generally, the original idea and design have to compromise to limitations or imperfections of each processing or manufacturing step of the workflow, which sometimes is called “design for manufacturing”.

The worse part is the workflow of additive manufacturing can be very long. This is the reason why we need “design for additive manufacturing” and better design tools and software.

We may be seeing AM design and design tools evolving fast as one of the development priority. The industry needs robust and powerful design methods and tools that enable users to design for the product instead of the process or additive manufacturing. With Dr. Lin Cheng, we are going to touch a little on the topic of Design & Optimization in the following weeks, where we will share strategic thinking on design, discuss cutting-edge developments and offer suggestions. Watch out for our next article at LinkedIn or our website!

Please like, comment or share if you find this article is interesting. 🙂

Thanks!

Runze

If your delta can reach positive through certain time with relatively high confidence, the disruption is happening and you should jump in; if your delta will be negative due to your competitors’ positive deltas in near future, the disruption is coming and you should be prepared; if your customers’/supplies’ delta will be positive but not yours, you need to find a way to lead the disruption to you.

If your delta can reach positive through certain time with relatively high confidence, the disruption is happening and you should jump in; if your delta will be negative due to your competitors’ positive deltas in near future, the disruption is coming and you should be prepared; if your customers’/supplies’ delta will be positive but not yours, you need to find a way to lead the disruption to you.